What Really Happens After Your Offer Gets Accepted | Homebuying Process Part 8

What Really Happens After Your Offer Gets Accepted

Most people think getting an offer accepted means the hard part is over. Nope. That is when the real work starts.

Finding the house, getting preapproved, picking a lender, dealing with listings, and trying not to lose your mind during the search, all of that matters. But once a seller says yes, now the machine starts moving. Escrow opens. The lender starts digging through your life again. Inspections happen. Appraisals happen. Deadlines start stacking up. Money starts moving. And everybody suddenly wants paperwork.

If you have not bought a home in a while, or you have never bought one before, this part can feel confusing because a lot of the important work happens behind the scenes. That is exactly why people get nervous. They do not see movement, so they assume nothing is happening. A lot is happening.

I want to walk through what actually happens after your offer gets accepted, what can go wrong, what your real estate agent is probably doing in the background, and what you need to pay attention to so you do not lose the house, lose time, or lose money.

🏠 Before escrow even starts, do not create your own problems

There is one issue I see all the time before buyers even get into the contract stage, and it can mess up the whole process.

You find two homes you love. Both feel right. Both check the boxes. You go home to think about it, talk to family, pray on it, sleep on it, whatever you need to do. Then one of them sells over the weekend.

Now the strange thing happens. A lot of people do not want the one that is still available anymore. They want to restart the entire search.

That sounds irrational until you understand what is going on. In your mind, you did not simply choose House B. You rejected House A. Once your brain frames it that way, House A stops feeling like a winner. It feels like the one you already passed on.

The better way to handle this is simple:

- Pick a first choice

- Pick a second choice

- Treat both as acceptable options

- Move quickly in competitive seasons

If your top choice gets away, you still have a real backup instead of emotionally blowing up your own search.

This matters even more in spring and early summer when homes move fast and agents are juggling multiple clients at once.

⏰ Why your agent may seem less responsive than you want

I am going to say something people do not always like hearing. Sometimes your agent is not ignoring you. Sometimes they are stuck with another client who is eating up far more time than they should.

Real estate is full of situations where someone calls late and wants immediate service, then gets upset because the agent already committed that block of time to another family. Or the agent is trying to leave one appointment to write an offer and the buyer wants to stand in the driveway talking for another 30 minutes about how much they love the house.

That stuff happens constantly.

So if your agent is delayed, late, or not answering in the exact second you want, the problem is not always laziness. A lot of times it is the reality of serving multiple people in a time-sensitive business.

That is also why decisiveness matters. If you know what you want, communicate clearly, and keep things moving, your transaction goes smoother.

💸 Lowball offers can backfire harder than people think

Yes, you can make a low offer. No law says you cannot. But that does not mean it is smart.

A lot of buyers think they can throw out an extreme number, get rejected, then come back with a normal one. Sometimes that works. Sometimes the seller is offended and refuses to deal with you at all.

That is the part people forget. Negotiation is not just math. It is emotion, timing, leverage, and how badly the other side wants to cooperate.

If a house is listed at $400,000 and you decide to test the waters at $300,000, do not be shocked if the seller decides they are done with you. On the flip side, in a multiple-offer situation, trying to save just $1,000 or $2,000 can cost you the whole house.

The right question is not, “Can I lowball?” The right question is, “How much do I want this house, and what is a realistic negotiation range?”

If you are buying in Las Vegas or anywhere else with active competition, being overly cute with your offer can be expensive.

🔐 What escrow actually is

Once your offer is accepted, you go into escrow.

Escrow is the neutral process that holds everything together while the transaction gets completed. At the end of it, the seller gets paid and you get the house.

That sounds simple, but there are multiple moving parts inside escrow:

- The escrow or title company opens the file

- Your deposit is collected

- The lender starts full loan processing

- Title work begins

- Inspections and appraisal happen

- Deadlines are tracked

- Final documents are prepared for signing

Here is something many buyers do not realize. Even though escrow companies are supposed to be neutral, there are business relationships in this industry that create pressure. Realtors, lenders, title reps, and escrow companies all work together regularly, and sometimes one side pushes hard to use “their” people.

Pricing is often similar, especially where rates are regulated, but incentives and loyalty can still affect how smooth or awkward a transaction feels.

This is one reason why understanding motivations matters. In real estate, motivations explain a lot.

📄 What happens with your loan after acceptance

Getting preapproved is not the same as getting fully approved.

After your offer is accepted, your agent sends the contract and transaction details to the lender. Then the lender starts the full process. This is where a lot of buyers get irritated because they feel like they are being asked for the same documents over and over again.

That is because they are.

Preapproval is the early pass. Full underwriting is the deep dive. The lender is now checking everything with more scrutiny. Income, assets, employment, debts, account activity, all of it.

And if you are working with a big lender, the point of contact may keep changing. First you talk to one person. Then it is processing. Then underwriting. Then another department. Local lenders often feel easier because you usually deal with one main person throughout the transaction.

That does not automatically make one better than the other, but it does affect the experience.

For general background on how mortgage underwriting works, the Consumer Financial Protection Bureau has a solid plain-English explanation.

Why loans can still get denied

Most preapproved buyers make it through just fine. Loan failures after preapproval are not common, but they do happen.

Some of the problems that can kill a deal include:

- Your job situation is not what the lender thought it was

- You are relocating and do not have confirmed employment approval for the move

- You defaulted on certain government-backed debt

- Your spouse has a federal default affecting eligibility on FHA or VA financing

- You spend money you needed for closing

That last one gets people more than it should. Do not go on vacation with your house money. Do not decide the appraisal offended you, then go empty your account. Do not make sudden financial moves during escrow unless your lender told you it is okay.

🧾 Appraisal and inspection are not the same thing

Buyers mix these up all the time.

The appraisal protects the lender. It is about value. If the home is not worth what you agreed to pay, the lender does not want to be overexposed.

The inspection protects you. It is about condition. The inspector is looking at the house, the visible systems, and anything accessible at the time of the inspection.

Those are two completely different jobs.

Also, home inspectors are not magicians and they are not there to take liability they do not need. They inspect what they can see and what they can safely test. If a light bulb is burnt out, many inspectors will not replace it just to see if the fixture works. If a fireplace needs a pilot lit, many will not touch it. If they cannot safely verify something, they note it.

That is not laziness. That is liability management.

If you are curious about what home inspections typically cover, the International Association of Certified Home Inspectors has a helpful overview.

Las Vegas-specific inspection reality

In Las Vegas, roof issues show up on reports all the time, especially on tile roofs. Wind, heat, and sun beat those roofs up. Cracked or shifted tiles are common. That does not automatically mean the roof is actively leaking or the whole thing needs replacement.

A lot of the time the actual fix is far smaller than the report makes it sound.

🛠️ What happens if the inspection finds problems

Once the inspection comes back, you usually have three broad outcomes:

- The seller agrees to fix the issues

- The seller offers money instead of doing repairs

- The seller refuses and you decide whether to proceed or cancel

Now let me be blunt. A lot of buyers are better off taking money or credits instead of trusting a seller repair.

Why? Because some sellers do the absolute cheapest, sloppiest repair job they can get away with. If they are mentally checked out of the house already, they may only be trying to get to closing, not do quality work.

So if you can negotiate a credit and handle the repair yourself after closing, that is often cleaner. Not always, but often.

🕵️ Due diligence means more than paperwork

During the due diligence period, usually around 7 to 10 days and sometimes longer for larger or more complicated homes, you have time to investigate what you are buying.

This is not just for inspections.

This is the time to:

- Read disclosures

- Review inspection results

- Check the neighborhood at different times of day

- Visit on weekdays and weekends

- Talk to neighbors

You would be amazed what neighbors will tell you. Sometimes they will happily give you the entire history of the block, including things the seller wishes nobody ever brought up again.

If the street is peaceful on Saturday afternoon but chaos on weeknights, you want to know that before you close. If there is a nuisance house nearby, you want to know that too.

Due diligence is your investigation window. Use it.

📘 HOA documents can give you an out

If the property is in an HOA, there is another important review period.

The seller has to get the HOA package ordered and delivered, and once you receive it, you usually have a limited number of days to review it. If you do not like the rules, fees, restrictions, or other HOA terms, you can often cancel during that review period.

And people cancel for all kinds of reasons. Parking restrictions alone can do it.

If you are buying in a homeowners association, read those documents carefully. The HUD home buying resources are also useful for understanding the broader purchase process and buyer responsibilities.

✍️ Getting to closing

As you get closer to closing, the lender sends your final loan documents. This is where you confirm the interest rate if it is locked, the payment, and the final numbers tied to the loan.

If your agent has experience reviewing loan paperwork, send them a copy and ask them to look it over. I always think another set of eyes is smart.

Then the title company prepares the final closing statement and signing package. After that, you sign.

If you are out of town, that usually is not a big deal. A mobile notary can come to you, handle signatures, and return the documents.

Once all signed documents are in, all money has been received, and the lender funds the loan, the package goes to the county recorder. In many places now, including Clark County, recording is electronic and much faster than it used to be.

And here is the answer to the question everybody asks over and over:

You get your keys when the transaction records.

Not when you sign. Not when money is “almost there.” Not when someone says it should happen soon. When it records.

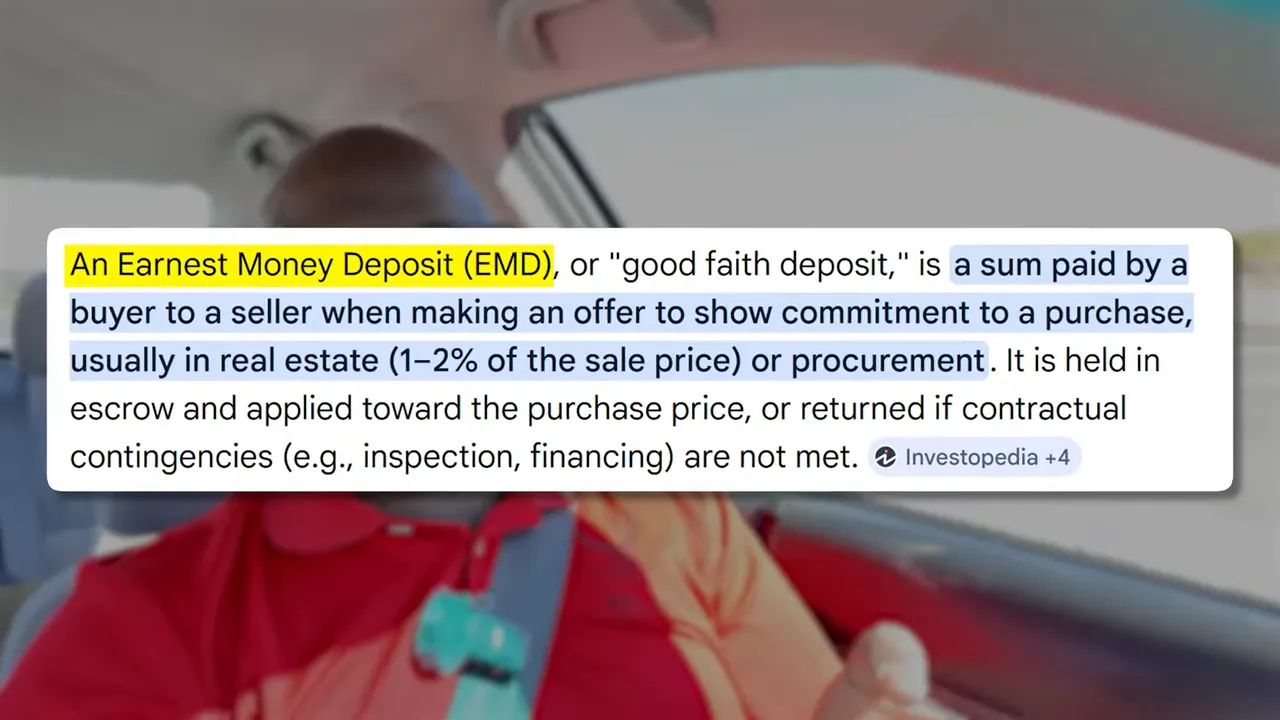

🔑 Earnest money deposit, explained plainly

Your earnest money deposit, or EMD, is your good-faith deposit. It shows you are serious.

It is commonly around 1 to 2 percent of the purchase price, though it can vary. On a $300,000 home, that might be around $3,000. On a more competitive listing, the seller may ask for more.

Here is what I want you to remember:

- The EMD amount is negotiable

- You do not have to blindly accept whatever the seller wants

- If the amount looks unusually high, pay attention

When a seller wants something way out of line, I get suspicious. Sometimes the plan is not to strengthen the deal. Sometimes the plan is to make it harder for you to get your money back if the transaction blows up.

How earnest money is paid

Normally the title company gives you wiring instructions. Follow those instructions carefully.

And yes, you usually need to send a wire. Not an ACH transfer because it is free. The wire fee might annoy you, but title companies often need it sent that specific way. Trying to save $35 can create a bigger problem than you think.

Also, wiring instructions should come from the title company, not from some random email that looks close enough. Wire fraud in real estate is a real thing. The FBI has warned repeatedly about real estate wire fraud, and this is one reason the industry has tightened up who sends what.

Your earnest money is not extra money on top of everything else. It is credited toward what you owe at closing.

⚖️ When can you get your earnest money back?

This is where people get confused, and sometimes get burned.

There are legitimate ways to cancel and still get your EMD back, depending on the contract and timeline. Common examples include:

- Canceling during the due diligence period

- Rejecting unacceptable HOA terms during the HOA review window

- An appraisal coming in low and no agreement being reached

- The loan not being approved within the contract terms

- Certain property-specific disclosures, such as solar-related forms, creating a cancellation right

For example, if a $500,000 contract appraises at $490,000, a few things can happen:

- You pay the difference

- The seller lowers the price

- You meet in the middle

- You cancel if your contract allows it

That is the clean version.

The messy version is this: even when you are entitled to your deposit back, escrow companies often want both sides to sign off before releasing the money. Most sellers will sign. Some will not.

That is where certain bad actors try to play games. They know you are probably entitled to the money, but they also know forcing you into arbitration or legal action creates hassle. So they try to pressure you into settling for less just to get the dispute over with.

That is one reason I pay close attention when I see unusually aggressive EMD demands. Sometimes that is not confidence. Sometimes that is setup.

🧠 Final thoughts on trusting the process without going blind

The post-acceptance part of home buying is busy, technical, and a little messy. That does not mean it is broken. It just means there are a lot of professionals, deadlines, documents, and legal requirements all trying to line up at once.

The smoother your transaction feels, the more likely it is that people behind the scenes are doing their jobs well.

What helps most?

- Be decisive before you offer

- Offer within reality, not fantasy

- Respond to lender requests quickly

- Do not touch your closing money

- Use your due diligence period wisely

- Read HOA and disclosure documents

- Understand when your deposit is protected and when it is at risk

- Remember that you get the keys only after recording

Home buying is not just about finding a pretty kitchen or a nice backyard. It is about managing a process correctly so you end up with the right house at the right terms without stepping on avoidable landmines.

And if this all feels like more than real estate school-level information, that is because it is. A lot of what actually matters in this business gets learned through experience, not the textbook version.

❓FAQ

When does the real work start in the homebuying process?

The real work starts after your offer is accepted. That is when escrow opens, the lender begins full underwriting, inspections and appraisal get scheduled, and closing deadlines begin.

Is preapproval the same as final loan approval?

No. Preapproval is an early review. Final approval happens later after the lender verifies your finances, employment, assets, and other details more thoroughly during underwriting.

What is the difference between an appraisal and an inspection?

An appraisal is for the lender and focuses on value. An inspection is for the buyer and focuses on the visible condition of the home and its systems.

Can I lose a house by making a lowball offer?

Yes. A seller may reject the offer and refuse to negotiate further. In a competitive market, even coming in slightly under what another buyer offers can cost you the deal.

How much earnest money do I usually need?

Often around 1 to 2 percent of the purchase price, though it varies by market, property, and negotiation. The amount is usually negotiable.

Do I get my earnest money back if the deal falls apart?

Sometimes, yes. It depends on the contract terms and why the deal ended. Common protections include due diligence, appraisal, loan, and HOA review contingencies, but the release process can still become a dispute if the seller refuses to sign off.

When do I get the keys to my new house?

You get the keys after the sale records with the county. Signing the documents is not the final step. Recording is.

Should I spend money or make big financial changes during escrow?

No. Avoid major purchases, account changes, job changes, or spending your closing funds unless your lender specifically tells you it is okay.

Categories

Recent Posts