Is the Las Vegas Housing Market About to Crash in 2026? | What Buyers and Sellers Need to Know Now

Is the Las Vegas Housing Market About to Crash in 2026? What Buyers and Sellers Need to Know Now

Everybody wants the same answer right now. Is the Las Vegas housing market about to roll over, or is this just a slower, more normal market after a wild run?

I understand the confusion. One headline says rates are improving. Another says inventory is rising. Then you hear prices are flat, homes are sitting longer, and suddenly people start throwing around the word crash like it means nothing.

It means something. And if you are planning to buy or sell in Las Vegas, using the wrong word can lead to the wrong move.

The good news is the actual data paints a much clearer picture than the headlines do. What I’m seeing in Las Vegas in 2026 is not a crash. It is a market that has cooled, stabilized, and become far more strategic. That creates opportunity, but only if you understand where the leverage is.

🏠 The national housing market is thawing, not surging

Las Vegas never moves in total isolation. National housing conditions affect mortgage rates, buyer confidence, inventory behavior, and affordability here at home.

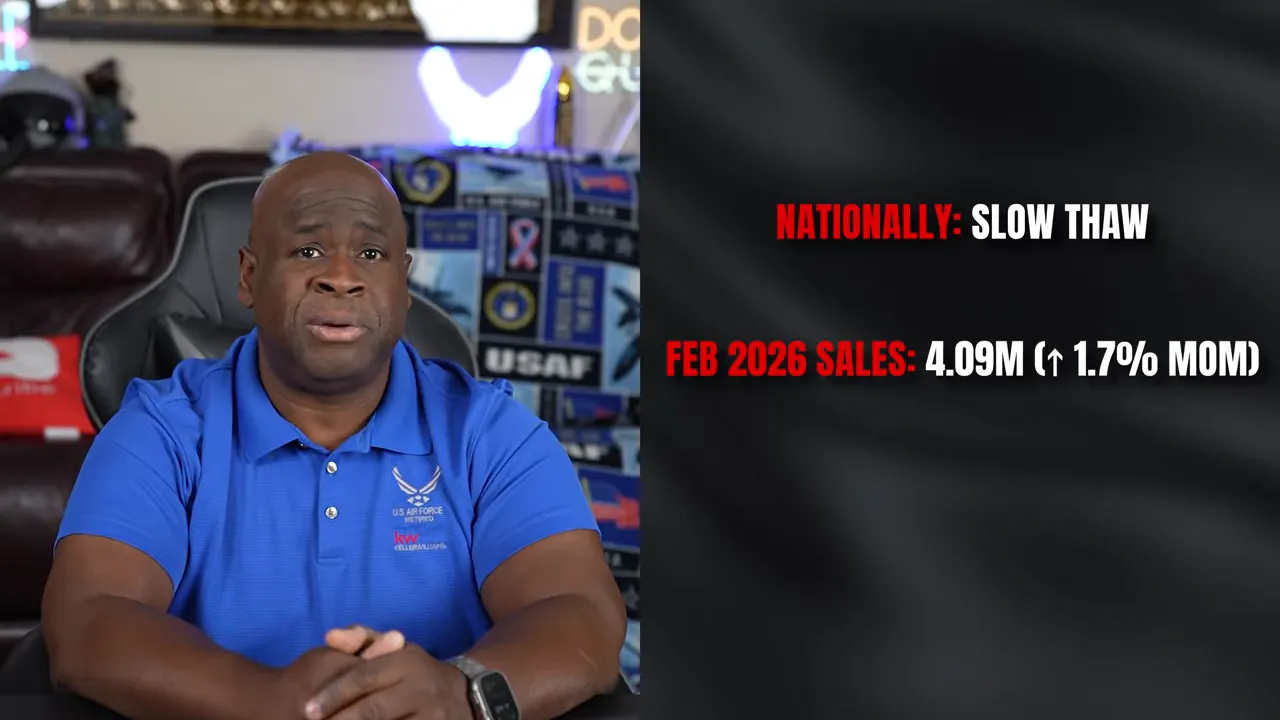

Across the country, existing home sales have started inching up after a very rough stretch. February came in at 4.09 million existing home sales, up 1.7% month over month. That sounds decent, but context matters. The last couple of years were among the slowest for home sales in recent history when adjusted for population.

So the broader U.S. market is not roaring back. It is slowly defrosting.

That matters because a slow national recovery tends to support a similar pattern in local markets like Las Vegas. It usually means less frenzy, fewer bidding wars, and more negotiation than people got used to during the pandemic years.

💸 Mortgage rates still matter more than almost anything else

If there is one force that continues to shape the housing market more than any other, it is mortgage rates.

Early in 2026, rates were hovering in the mid-6% range, with Freddie Mac reporting around 6.37% at one point. Not long before that, rates briefly dipped under 6%, touching 5.99%. That was the most favorable rate environment buyers had seen in quite a while. Then global instability and rising oil prices pushed rates back up again.

This is a good reminder that mortgage rates do not move only because of housing. They react to bond markets, inflation expectations, and geopolitical events too. That can create fast swings in affordability.

And affordability is not some abstract concept. It shows up in the monthly payment.

- A $500,000 loan at 6.45% comes out to about $3,144 per month in principal and interest.

- The same loan at 7.26% would be roughly $3,414 per month.

- That is about $270 per month in savings.

That difference is real. It can change what neighborhood someone can afford, whether they can qualify at all, or whether buying makes more sense than waiting.

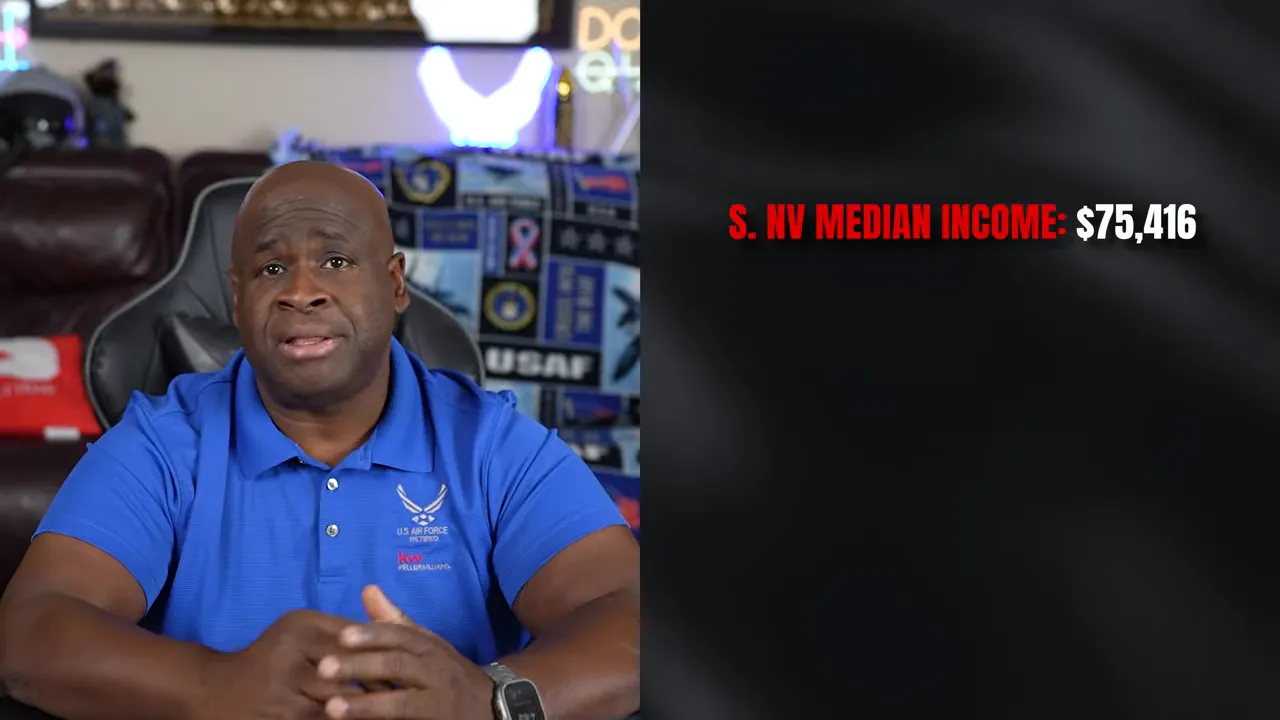

There is also a positive trend that deserves more attention. In Southern Nevada, household income has been rising faster than home prices. The median household income is now about $75,416, up close to 10% year over year and more than 21% over the last five years.

When incomes rise faster than prices, affordability improves over time. It does not solve everything, but it is a healthy signal.

📊 Single-family home prices in Las Vegas are stabilizing

Now let’s talk about the numbers that really matter on the ground.

For single-family detached homes in Las Vegas, the median sales price is $480,000. That is down about 1% from the same time last year and basically flat from the prior month.

That is not what a crash looks like.

A crashing market usually shows steep price declines, fast deterioration in demand, and forced selling. What we have instead is stability. Prices are no longer sprinting upward, but they are not falling apart either.

Sales activity also tells an important story. In March, 2,288 single-family homes closed, which was nearly 7% higher than the same period a year ago. That means buyers are still active. They are just more selective and more price sensitive.

Inventory has risen, but not because there is some giant wave of panicked sellers. There were 6,456 active single-family homes on the market without pending offers, up 19.2% year over year. New listings in March totaled 3,367, which was basically unchanged from last year.

So if new listings are flat but total inventory is rising, that usually means homes are taking longer to sell.

That is exactly what is happening.

Back in 2021, most active listings were brand new to the market. Today, only about 36% of active listings are fresh. The rest have been sitting and waiting.

The effective inventory level for single-family homes is 2.8 months. A balanced market is generally considered somewhere around 4 to 6 months. That means Las Vegas is still technically in seller’s market territory for detached homes, just nowhere near the intensity of the last few years.

Another interesting sign of seasonal strength is that 54.5% of single-family homes are selling within 30 days. That is up from 47.6% the month before. Spring has brought some energy back into the market.

Still, not every listing is moving. About 11% of homes are sitting for more than 120 days, and in most cases that points back to one problem: price.

As for price per square foot, the valley ranges roughly from $240 to $276 depending on area, while premium communities like Summerlin and Henderson can go much higher, especially in the luxury space.

🏘️ Condos and townhomes are giving buyers more room to negotiate

If you are looking for the part of the Las Vegas market where buyers have the most leverage right now, this is it.

The condo and townhome segment has softened more than single-family homes.

- Median price: $295,000

- Year-over-year price change: down 3.8%

- March closings: 518, down 9.1%

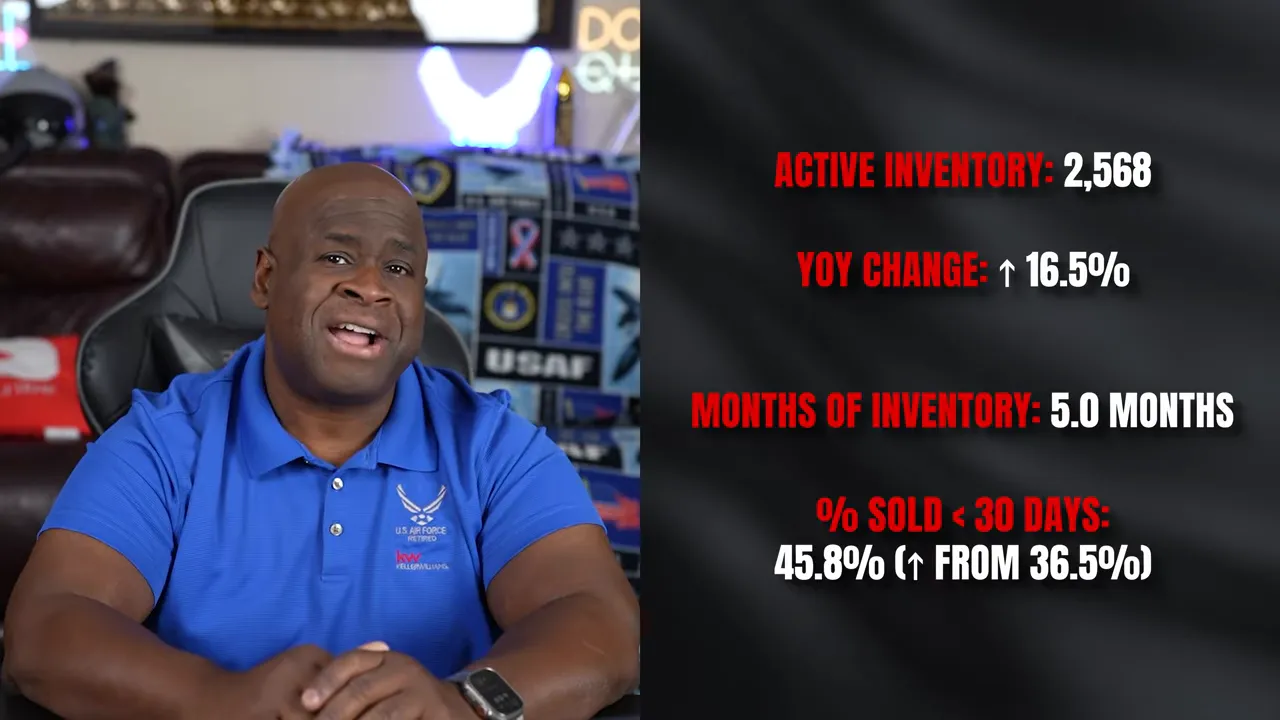

- Inventory: 2,568 units, up 16.5%

- Months of inventory: 5 months

That 5-month supply puts condos and townhomes right on the edge of a balanced market and leaning toward buyers.

Roughly 45.8% of condos and townhomes sold within 30 days, up sharply from the month before. So even here, spring demand is helping. But this segment clearly offers more negotiating room than detached homes.

For first-time buyers, downsizers, or anyone trying to enter the Las Vegas market at a lower price point, this category deserves serious attention. There are more options, less urgency, and better chances to negotiate repairs, concessions, or price.

🎯 Sellers need precision pricing, not wishful thinking

This is the most important part of the whole conversation for sellers.

In this market, pricing right from the beginning is not a nice idea. It is the strategy.

Right now, 41% of active listings in Clark County have already reduced their asking price at least once. That means nearly half the market started too high.

And the performance gap between properly priced homes and overpriced homes is not small. It is huge.

Homes that sold without any price reduction:

- Made up 64% of recent sales

- Sold in a median of 14 days

- Got 99.4% of asking price

Homes that reduced price by 1% to 4%:

- Took around 60 days to sell

- Got 98.8% of final asking price

- But only 96.2% of the original asking price

One example showed a home that started at $616,000, dropped to $600,000, and finally sold for $593,000. Starting too high cost that seller about $23,000 from the original ask.

Homes that reduced by 5% or more:

- Sat around 98 days

- Only got about 96% of original asking price

In another example, a seller started at $651,000, reduced to $600,000, and sold at $590,000. That is a $61,000 haircut from where they began.

The pattern is obvious. Overpricing does not create leverage. It kills momentum.

And momentum matters. About 25% of homes that sold in the first three weeks went above asking price. For homes sitting two months, only 13% sold above asking.

The longer a home sits, the more buyers start wondering what is wrong with it. Once that happens, seller leverage fades fast.

🌆 The Las Vegas economy is still providing real support

Real estate follows jobs, population growth, income, and confidence. By those measures, Las Vegas still has a solid foundation.

Clark County added nearly 45,000 residents over the past year, pushing the population above 2.4 million. A big portion of those new residents continue to come from California. That migration trend matters because it brings demand, purchasing power, and lifestyle-driven relocation into the valley.

Why do people keep coming? A few reasons stand out:

- Zero state income tax in Nevada

- Relative affordability compared to major coastal markets

- Lifestyle and weather

- Long-term development across the valley

Southern Nevada’s economy also showed meaningful growth. Gross domestic product rose 6.1% in 2024 to nearly $196 billion. Employment sits around 1.148 million jobs, and unemployment has moved down to 5.2%.

Tourism did soften, with visitor volume down 7.5% in 2025, but gaming revenue in Clark County still held up at about $13.7 billion, slightly above the prior year.

And then there is the development pipeline. Las Vegas is still building.

- A new Major League Baseball stadium project tied to the Athletics

- The Brightline West rail connection toward Southern California

- The Hard Rock transformation of the Mirage

- Billions more in projects under construction or planned

That kind of investment does not guarantee price growth every year, but it does support the long-term outlook.

For broader economic context, resources like the FRED economic database and the Freddie Mac mortgage market survey are useful if you want to track rates and market trends beyond local headlines.

🚨 So, is a Las Vegas housing crash coming?

Short answer: no.

At least not based on the conditions that normally create a true housing crash.

To get a real crash, I look for three things happening at the same time:

- Weak buyer demand

- Major oversupply of homes

- Large numbers of desperate or forced sellers

Right now, Las Vegas only checks one of those boxes, and even that one is partial. Buyer demand is softer than it was during the frenzy years because rates are higher. But the other two ingredients are missing.

There is no major supply glut. Inventory is up, yes, but it is still low by historical standards. Nationally, there are about 1.3 million homes on the market. During the Great Recession, that number was closer to 4 million.

That is not a small difference. That is a completely different environment.

And sellers are not broadly distressed. Around 70% of homeowners in the U.S. have mortgage rates of 5% or below. They are not eager to give up those loans unless they truly need to move.

On top of that, equity positions are strong:

- More than 91% of homeowners have at least 25% equity

- More than 76% have over 40% equity

People with that kind of equity are not trapped. They are not sitting on the edge of foreclosure the way many owners were in the last housing collapse.

Foreclosure filings have risen from the unusually low pandemic period, but they are still about 25% below 2019 levels and nowhere close to Great Recession territory. Locally, distressed properties make up only about 1.7% of the market.

That is a cooling market. Not a crash market.

🛒 What buyers should do right now

If you are buying in Las Vegas in 2026, you have more negotiating power than buyers have had in years. Do not waste it.

Here is how I would approach this market.

Use your leverage

Inventory is up, listings are sitting longer, and sellers are more open to talking. If a property has been on the market for more than 30 days, there is a good chance you can negotiate.

That may include:

- An offer below asking price

- Seller-paid closing costs

- An interest rate buydown

- Repair credits or other concessions

Do not obsess over perfect timing

A lot of people say they are waiting until rates fall to 5%. I understand the logic, but there is a catch. Lower rates usually bring more buyers back into the market. More buyers often mean more competition, stronger prices, and fewer concessions.

The leverage you have today could shrink quickly if rates come down and demand surges.

Look where the value is

Condos and townhomes offer some of the best deals right now. North Las Vegas also offers more attainable entry pricing, around the mid-$400,000 range in some cases.

And do not ignore builders. New construction communities are often offering aggressive incentives, including rate buydowns into the low 5% range and sometimes even lower, plus upgrades and closing cost help.

🏷️ What sellers should do right now

You can absolutely sell successfully in this market. But this is no longer the era where any number on the sign works.

Buyers today are informed. They compare everything. They know recent sales, they know what is sitting, and they know when a seller is reaching.

If I were selling in Las Vegas right now, I would focus on four things:

- Price the home correctly from day one. Use the most recent comparable sales, not the dream number from two years ago.

- Work with someone who knows the neighborhood. Hyper-local pricing matters more in a slower market.

- Make the home show well. Clean it, declutter it, repair what is broken, and freshen up paint if needed.

- Win online first. Photos matter because buyers often decide whether a home is worth seeing based on the digital presentation alone.

When a home is priced right and presented well, it can still move quickly and close near full asking price. When it is overpriced, it usually sits, gets ignored, then chases the market downward.

⚖️ The real 2026 Las Vegas market outlook

The Las Vegas housing market in 2026 is neither falling apart nor flying off the rails to the upside.

It is finding balance.

That balance is important because it creates different kinds of opportunity for different people.

For buyers: more choices, more negotiating power, and better odds of getting concessions.

For sellers: strong outcomes are still available, but only with discipline, preparation, and pricing precision.

If you want the simplest summary possible, here it is:

- Single-family homes are stable and still lean seller-friendly

- Condos and townhomes offer stronger buyer leverage

- Rates remain the biggest wildcard

- Overpricing is getting punished

- A true crash is not supported by the current data

❓FAQ

Is the Las Vegas housing market crashing in 2026?

No. Prices are mostly stable, inventory is rising in a manageable way, and there is no widespread evidence of forced selling or foreclosure-driven distress.

Are Las Vegas home prices dropping?

Single-family home prices are essentially flat, with the median around $480,000 and down about 1% year over year. Condos and townhomes have softened more, with prices down about 3.8%.

Is Las Vegas a buyer’s market right now?

For single-family homes, it is still technically a seller’s market with 2.8 months of inventory, though much softer than before. For condos and townhomes, the market is much closer to balanced and leans more in the buyer’s favor.

Should I wait for mortgage rates to drop before buying in Las Vegas?

Waiting for lower rates can backfire if more buyers jump in at the same time. Lower rates often increase competition and reduce negotiating power. If the home and payment work today, buying now and refinancing later can be a smart move.

What is the biggest mistake Las Vegas sellers are making right now?

Overpricing. Homes that start too high tend to sit longer, require price cuts, and often sell for less than they would have if they had been priced accurately from the start.

What areas or property types offer the best value in Las Vegas right now?

Condos, townhomes, and some entry-level homes in North Las Vegas currently offer stronger negotiating opportunities. New construction is also worth a hard look because many builders are offering rate buydowns and incentive packages.

If you are trying to make a move in Las Vegas, this is the kind of market where strategy matters more than speed. The people who do best are not the ones waiting for perfect conditions. They are the ones making well-informed decisions based on what the market is actually doing right now.

Categories

Recent Posts