The Truth About Real Estate Market Spin

The Truth About Real Estate Market Spin

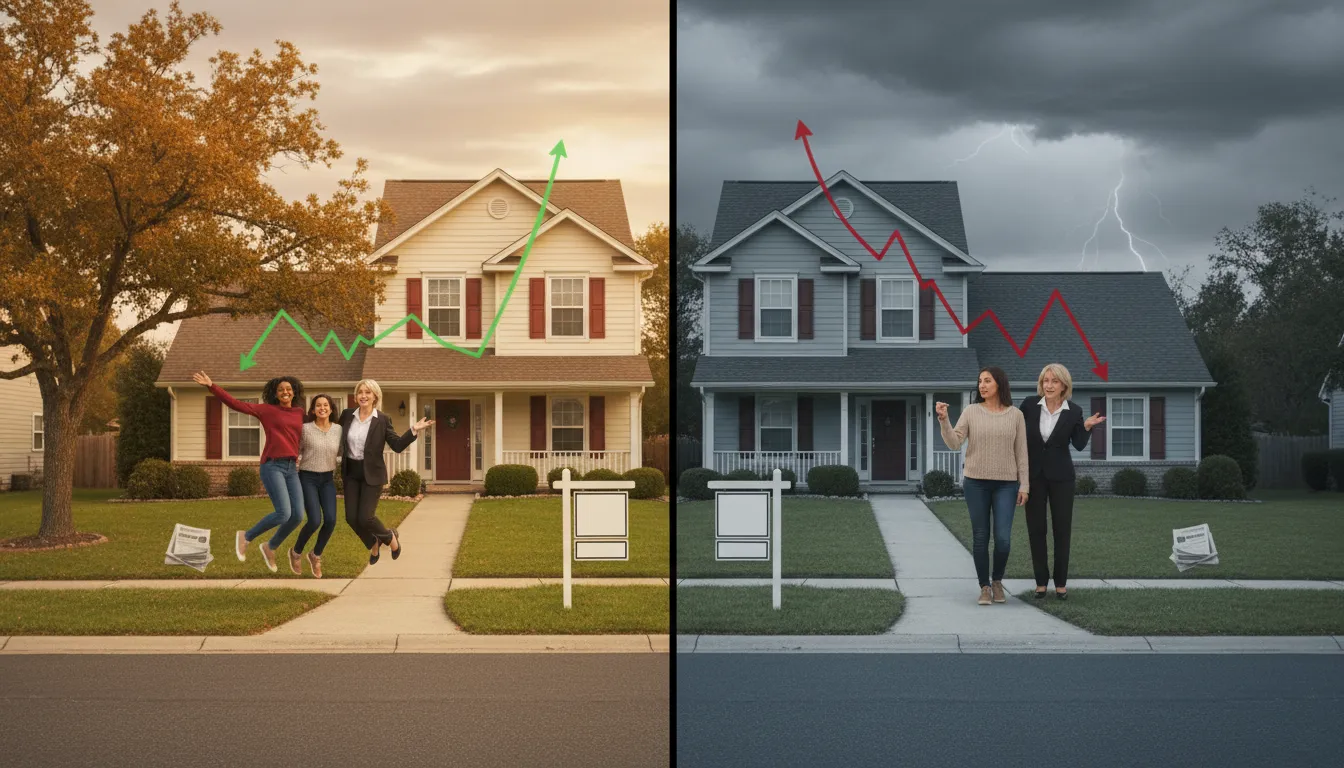

I get asked a lot why one realtor says the market is booming while another says it is crashing. The short answer is simple: the same facts can be framed in wildly different ways depending on the story someone wants to tell. I’ll walk you through how market data gets spun, why buyers and sellers hear different things, and what to look for so you can make better decisions instead of reacting to the headline of the day.

📊 Liars, statisticians, and the power of framing

There’s an old line: liars, damn liars, and statisticians. I’d add politicians and headline writers to that list. The truth is you can present accurate numbers and still lead people to completely opposite conclusions. A single statistic viewed in isolation rarely tells the whole story.

Example: you might see a headline that says 53 percent of American households saw their home value drop last month. That can be 100 percent true. But you could also say the average homeowner doubled their equity over a multi-year period. That might also be true. Which headline gets clicks depends on who is trying to attract attention and for what purpose.

Rule of thumb: always ask two follow-up questions when you see a dramatic market stat — (1) what baseline are they using, and (2) what time period are they comparing?

🏠 The delta matters more than the month-over-month headline

People emotionally react when their asset loses value in a single month. If a house goes from $500,000 to $480,000 they hear they “lost $20,000.” But that ignores where the homeowner started.

I use a simple example all the time: say you bought a home in 2012 for $130,000. Today it’s worth $500,000. If it dips to $480,000 next month, you technically lost $20,000 on paper — but you still gained $350,000 over your purchase price. That context changes the meaning completely.

When people focus on a single negative monthly movement without considering the purchase price or multi-year trend, they miss the real picture. The important number for most homeowners is the delta between purchase price and current value, not the tiny swings month to month.

📉 Tale of two houses: timing is everything

I once had two guys in my squadron with similar houses but very different outcomes. One bought at the bottom in 2012. The other bought earlier in 2010. Fast forward a few years: the 2012 buyer walked away with a big profit because he bought at the market low. The 2010 buyer expected the same payoff and was upset when his sale didn’t match his friend’s. He was comparing outcomes without comparing buy-in points.

That story illustrates a key point: when you bought matters as much as what a house is worth today. If you buy near a trough, you’ve got a head start. If you buy when the market is higher, your gains will look different even if you’re selling in the same month.

🧠 Cognitive bias: why negative headlines attract buyers

People who want to buy tend to look for confirmation that now is the time to buy. Negative headlines help them justify that belief. Sellers want to hear everything is great so they feel comfortable listing. That’s why you’ll see different spins from different sources.

Negative stories generate clicks and phone calls. Buyers will call based purely on a negative video or headline because it matches their hope of buying at bargain prices. The flip side is sellers will chase optimistic headlines to justify asking top dollar.

🔍 Foreclosures and probates: outdated expectations

There’s a persistent myth that you can buy foreclosures for pennies on the dollar. That used to be closer to the truth during or right after the housing crash when programs like HARP and HAMP were in place and the government effectively subsidized banks to clear inventory.

Today those programs are gone. Asset managers and banks are turning over foreclosures for market value. Real foreclosures are rare. In a month with thousands of sales, you might see half a dozen true bank-owned properties. Probate sales are similar — the courts and asset managers aim to collect fair market value, not give away homes.

Bottom line: don’t plan your strategy around old foreclosure myths. Expect competition and pricing closer to market than to “discounted” levels.

🕰 Expectations in a normal market

People keep calling the current market “crashing” when what’s really happening is a shift back to normal. A couple of years ago homes were selling in days. Today a well-priced home in many markets will take 40 to 66 days to sell. Two years ago 14 days felt normal to buyers and sellers. But 25 years ago listings sat for 120 days in many places.

When you haven’t experienced a normal market in a generation, a return to normal feels like a crash. It isn’t. It’s a recalibration. Sellers who insist on pricing based on boom-era comps will see their listings linger, and many are pulling homes off the market rather than lower price expectations.

🔁 How different narratives get created

Here’s the pattern I see all the time:

- Negative spin to attract buyers: Highlight monthly declines, emphasize scarcity of deals, and push foreclosure myths.

- Positive spin to attract sellers: Focus on long-term appreciation, median price gains over years, and examples of big payouts to early buyers.

- Curated data: Both sides use true numbers, but selectively. They don’t always present the full baseline, timeframe, or local context.

It’s marketing. It works. Negative videos get views and phone calls. Positive messages get listings. Neutral, balanced information rarely drives the same engagement, even though neutral is what most people actually need.

⚖️ The complete picture matters

I’ll give you a blunt piece of advice: when you hear a dramatic market claim, ask for the complete picture. Some stories are like showing a cropped photo of an Iraqi prisoner — one outlet shows him being given water, another shows a soldier pointing a gun, and both omit the context that explains why both images exist.

Good data always needs context. Ask for:

- Timeframe: month-over-month, year-over-year, or decade-long?

- Baseline: who are they comparing — median, average, or a specific cohort?

- Local factors: is this national, state, county, or neighborhood-level data?

- Transaction types: retail sales, foreclosure inventory, bank-owned, or investor flips?

🛠 Practical steps: how to read the spin and act smart

If you want to make a practical, confident decision instead of reacting to headlines, here’s a checklist I use and recommend:

- Look at the purchase price and your equity. The delta is the real story for homeowners.

- Check multiple timeframes. Month-over-month moves can be noise. Year-over-year and multi-year trends reveal direction.

- Ask for local comps and days on market. A “market crash” will look different in every ZIP code.

- Ignore outdated foreclosure advice. Expect competitive pricing for bank-owned and probate sales.

- Calibrate expectations to a normal market. If 60 days is normal now, pricing to sell in 7 days is unrealistic.

- Find a trusted pro who explains context, not just headlines. Good advice saves both time and money.

🧾 Common scenarios and candid advice

Here are some situations I run into and what I tell people:

- Buyer expecting big discounts from “crash” headlines: Don’t count on national headlines to produce local bargains. Look for properties priced correctly for condition and location.

- Seller demanding boom-era returns: If comps show your neighborhood has cooled, adjust price expectations. Listing high just to wait is a cost you bear.

- Someone angling for a foreclosure deal: True foreclosures are rare and often priced to market by asset managers. Prepare for market-level competition.

🔎 Example scripts: what to ask your agent

If you want to cut through spin, try asking these direct questions:

- “Can you show me the 1-, 3-, and 5-year median price trend for my neighborhood?”

- “What was the purchase price of this home and how does that compare to current value?”

- “How many true bank-owned or probate sales closed here last month?”

- “What’s the average days on market for similar homes in the past 90 days?”

🧾 A short reality check

"It’s not what you make, it’s what you get to keep."

That old advertising line applies perfectly to real estate headlines. What matters is the net result for you — your equity, your financing, your timeline. Headlines are designed to trigger emotion, not to give you a financial plan.

🔁 Final thoughts: spin tells you who they want to attract

If a headline screams the market is crashing, the creator is probably trying to attract buyers. If the story is all rosy, it might be aimed at sellers. Neither is inherently dishonest — both are marketing. The bad part is when people take a single narrative as the whole truth.

I prefer to focus on practical, local, and time-tested indicators. That’s how you move from reacting to headlines to making decisions that actually meet your goals.

❓ Frequently Asked Questions

Why do realtors give opposite advice about the same market?

They are often framing true data to attract a specific audience. Negative framing attracts buyers; positive framing attracts sellers. Both can be factually correct, but they omit context like purchase price, timeframe, and local differences.

If my home's value dropped this month, should I panic?

No. Monthly swings are common. Evaluate the delta between what you paid and current value, review year-over-year trends, and consider your timeline. Short-term paper losses are not the same as a long-term loss.

Can I still find bargains in foreclosures?

Not the way you could a decade ago. Government programs that cleared bank inventories are gone. True foreclosures are rare and typically managed to recover market value. Bargains still exist, but you should not rely on foreclosure myths.

What is a "normal" market right now?

Normal means listings take weeks or months rather than days. In many areas 40 to 66 days on market is typical today. That feels slow to people used to ultra-fast sales, but it is a return to more typical cycles.

How can I protect myself from misleading market headlines?

Ask for context. Request local, multi-year trends. Focus on purchase price, equity, and days on market. Work with a professional who explains the full story instead of relying on a single clickbait stat.

📌 Practical next steps

When you see a dramatic headline, pause and follow the checklist from earlier. If you are buying, look for well-priced homes and realistic financing. If you are selling, price to the current market and factor in normal days on market so your timeline and expectations align.

Spin will always be part of the conversation. Learn to read it. Ask the right questions. Focus on your delta and your plan. That’s how you win, no matter what the headline says.

If you want a concise neighborhood trend or an honest read on a property, ask for the data that answers the baseline and timeframe questions. Good information beats spin every time.

Categories

Recent Posts