5 Mistakes First Time Buyers Made in 2025 and How to Avoid Them in 2026

5 Mistakes First Time Buyers Made in 2025 and How to Avoid Them in 2026

I saw the fallout last year up close: good people, steady jobs, real down payments, and still — one misstep and everything unraveled. Some lost homes they loved. Some drained their savings. Others walked straight into financial stress they never saw coming. Most of them thought they were doing everything right. That’s the dangerous part.

If you plan to buy a home in Las Vegas in 2026, you can avoid the same traps. Below I break down the five biggest mistakes first time buyers made in 2025, why they hurt so badly, and exactly what I tell buyers to do instead. I’m writing this from experience working with military families and civilians across the valley, and I want you to be prepared — not surprised.

🏁 Mistake #1 — Skipping pre-approval or getting it too late

The single heartbreak I saw most often was a buyer falling in love with a house and then learning the property was already under contract because they didn’t have a pre-approval. In Las Vegas, nearly half of homes still sell in under 30 days. If your offer isn’t backed by a pre-approval letter, it’s invisible to sellers.

Pre-approval is not paperwork for paperwork’s sake. Think of it as your financial GPS. It tells you your true budget, reveals hidden issues in your credit or debt-to-income ratio, and gives you the power to act immediately. That speed matters. When the right house hits the market, hesitation costs you the home and often tens of thousands of dollars in opportunity.

My practical pre-approval checklist:

- Get pre-approved before you tour homes. Do it weeks before you start looking, not after you’ve found “the one.”

- Provide full documentation. Pay stubs, W-2s, bank statements, and explanations for any large deposits.

- Ask the lender what you qualify for vs. what you should afford. The bank gives a ceiling; you pick a comfortable payment.

- Use your pre-approval to improve your position. If credit or debt is holding you back, your lender can suggest specific actions to boost your terms.

⏳ Mistake #2 — Waiting for the perfect market timing

<img src="https://firebasestorage.googleapis.com/v0/b/videotoblog-35c6e.appspot.com/o/%2Fusers%2FjWHHxVz9lPhTWobyNsW7yxwtk3V2%2Fblogs%2FZJrYg2NxekXn3DSSM7Ls%2Fscreenshots%2F413bec44-edae-46b2-82bd-097950fed5e3.webp?alt=media&token=084f3816-5e7d-4631-aa66-ef7b7576f84c" alt="Video title slide reading 'MISTAKE #2 WAITING FOR THE " perfect"="" time'="" over="" a="" blurred="" presenter"="" width="100%" style="object-fit: cover;">

Trying to time the housing market is like chasing a single raindrop in a thunderstorm — messy and unpredictable. In 2025 many buyers sat on the sidelines, waiting for a crash that never arrived. Meanwhile, Las Vegas prices continued to climb: median single-family prices rose about 2% and condos in areas like downtown and the Arts District jumped almost 7% late in the year.

The right time to buy is when you are ready, not when a talking head declares the bottom. Ask yourself the meaningful questions:

- Do I have stable income?

- Have I saved for a down payment and closing costs?

- Am I planning to stay in the area for at least a few years?

If the answers are yes, then buying can make more sense than waiting. Real estate rewards people who enter the game with a plan, not those who wait for perfect headlines.

💸 Mistake #3 — Underestimating the true cost of homeownership

A pre-approval number can feel like a green light to splurge. Don’t confuse the lender’s number with what you should be spending. The bank’s figure is a maximum; your comfort zone is smaller.

In 2025 many buyers discovered that the monthly mortgage payment was just the start. With interest rates elevated, people were house poor — a beautiful home but no money left for life. You must budget for:

- Mortgage principal and interest

- Property taxes and homeowners insurance

- HOA fees — in communities like Summerlin and Henderson these can be significant

- Maintenance and repairs — plan to save at least 1% of the home's value per year

- Utilities, landscaping, and routine replacements

I built my own purchases around a future reality — I based one home purchase on my projected retirement income so I could feel comfortable long term. That’s the mindset to adopt: buy a lifestyle you can afford today and years from now.

⚔️ Mistake #4 — Misjudging competition and offering too timidly

When the headlines say the market is cooling some buyers assume they can stroll in with lowball offers and dictatorial terms. That doesn’t work on well-priced homes in desirable neighborhoods like Green Valley or Centennial Hills. Good listings still attract multiple interested buyers.

Hesitation is often as costly as overpaying. I watched buyers hesitate for a weekend and lose a house by Monday. Preparation and timing beat procrastination every time.

How to make an offer that wins without overpaying:

- Lead with a clean, realistic offer. Being the highest price isn’t always necessary, but being the most reliable is.

- Match the seller’s timeline. Offer to close when it suits them or propose flexible move dates.

- Show commitment. A strong earnest money deposit and a solid pre-approval signal seriousness.

- Make contingencies reasonable and clear. A well-structured offer with meaningful contingencies beats a messy, uncertain one.

🔍 Mistake #5 — Waiving the home inspection

Skipping an inspection to make your offer more attractive is gambling with your life savings. In heated negotiations, buyers convinced themselves they would save time by waving inspection. Then a month after move-in they found a structural leak, a failing foundation beam, or other expensive surprises.

Never waive the inspection. Even in markets where buyers commonly waived them, I often found there remained a way to inspect and renegotiate. The inspection is your single best tool against a financial nightmare.

My inspection rules:

- Always get a full inspection. Every property, unless you have an extraordinary reason and deep pockets.

- New construction still needs inspection. Builders are human; they make mistakes. I recommend two inspections on new builds: one before closing and another around month ten to catch items that may emerge after occupation.

- Use the report strategically. Request repairs, a seller credit, or an adjustment. If a deal hides catastrophic issues, be ready to walk.

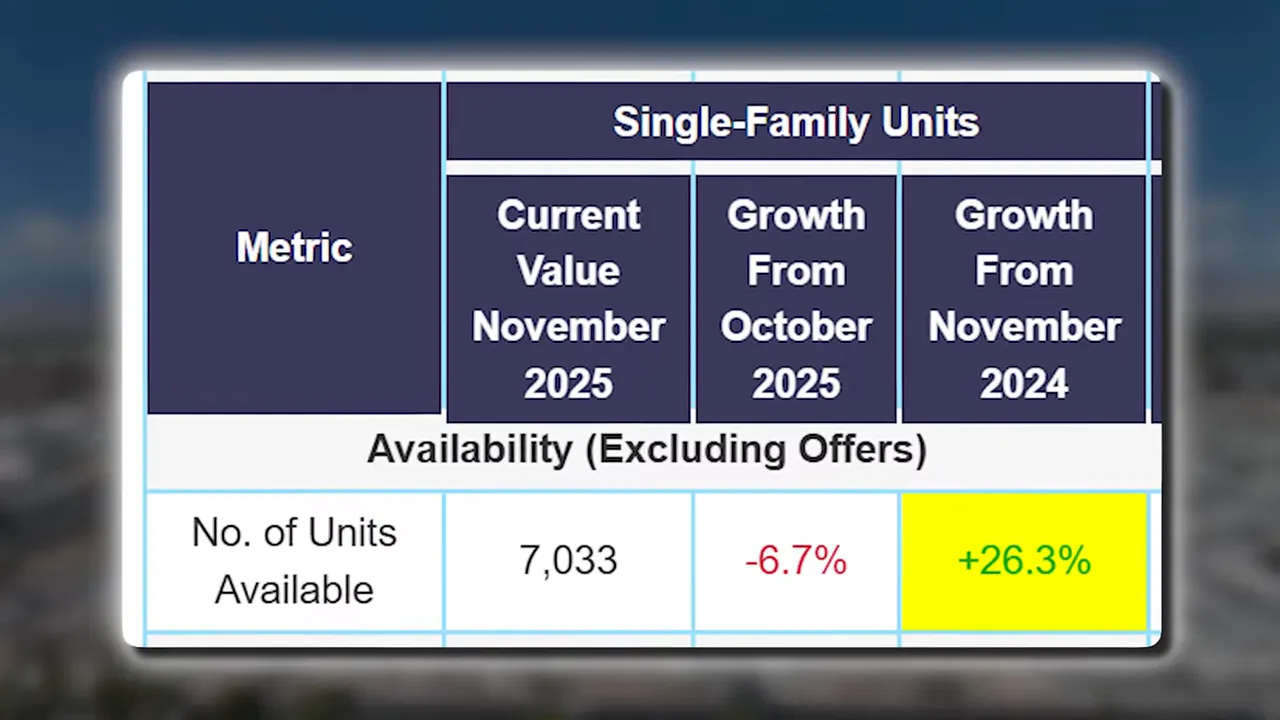

📈 Las Vegas market snapshot for 2026

Right now Las Vegas offers a rare window of opportunity. Inventory is up over 25% compared to last year, which means you have choices. You don’t need to settle for leftover scraps.

A few important dynamics to keep in mind:

- Prices are still rising, but more slowly. That gives buyers negotiating room without the chaos of bidding wars.

- Interest rates are easing. The Fed has started cutting, and borrowing costs are trending down. As rates drop more buyers return, and the market can heat up fast.

- This window won’t remain open forever. Easier rates plus more buyers off the sidelines could reset demand quickly — think of 2021 before the next big jump.

If you’re serious about buying in Las Vegas, now is a time to prepare and act. Inventory and price stability give you bargaining power you might not see again soon.

🧭 My 8-step action plan to buy smart in 2026

Use this as your checklist. These are the steps that separate buyers who sleep at night from buyers who call me six months later asking what to do.

- Get pre-approved early. Start with a lender who will actually review your financials and give practical advice, not just a number from a calculator.

- Create a total cost budget. Include mortgage, taxes, insurance, HOA, maintenance, utilities, and a 1% per-year maintenance fund.

- Decide your comfortable payment, not the bank's maximum. That gap protects you if rates change or unexpected repairs appear.

- Find an agent who knows your neighborhoods. Local knowledge about builders, neighborhoods like Summerlin, Green Valley, or Centennial Hills, and the military relocation process matters.

- Be prepared to move quickly. Have documents ready, a clear offer strategy, and flexibility on timelines when needed.

- Inspections are mandatory. Never waive them. For new builds, plan one before closing and another around month ten.

- Negotiate smartly. Structure offers that match what sellers want: clean contracts, reasonable contingencies, and realistic timelines.

- Plan for life after closing. Keep an emergency fund, budget for furnishing and small renovations, and don’t spend down to your monthly minimums.

📌 Quick reference: What to ask your lender and inspector

- To your lender: What loan programs fit my timeline? How can I improve my rate? What will my monthly cash flow look like including taxes and insurance?

- To your inspector: What are the top 3 maintenance items I should budget for this year? Are there any safety concerns? For new builds, what items commonly come up at the 10-month mark?

❓ FAQ — Common questions I get from buyers

How soon should I get pre-approved before house hunting?

As early as possible — ideally weeks before you start touring homes. Being pre-approved lets you shop confidently and makes your offer visible to sellers the moment the right house hits the market.

Is it ever okay to waive an inspection to win a bid?

No. Skipping the inspection is a risky gamble. If you need to make a stronger offer, consider other terms like earnest money, flexible closing dates, or seller credits rather than sacrificing the inspection.

How much should I budget for maintenance?

A solid rule of thumb is to set aside at least 1% of the home’s value per year for maintenance. Older homes or properties with big yards will require more.

What should I do if I can’t match other buyers’ offer prices?

Offer strength comes from reliability, not just price. A clean contract, quick verification documents, flexibility on closing dates, and a larger earnest money deposit can make your offer competitive without overpaying.

Do I need two inspections for new construction?

I recommend it. One inspection before closing catches immediate concerns. A second inspection around month ten can identify items that appear after settling in and before warranties expire.

How long will the current Las Vegas buying window last?

No one has a crystal ball, but inventory is higher now and price appreciation has slowed. As interest rates ease further and more buyers return, competition could ramp up quickly. If you’re ready, prepare now.

🏁 Final thoughts

Buying a home is one of the biggest financial decisions most people make. In 2025 I watched smart people make avoidable errors. In 2026 you can be different: get pre-approved early, buy when your life says yes, budget realistically, act decisively, and never skip the inspection.

The Las Vegas market is offering choices right now. Use them. Prepare so you can move when opportunity knocks, and don’t let fear of market timing keep you from building long-term wealth and a stable life.

If you want help building a plan tailored to your situation — especially if you're relocating or part of the military moving to Nellis or Creech — get a lender pre-approved, make a realistic budget, and reach out to someone who knows the neighborhoods and builders here.

Good luck. Make 2026 the year you buy wisely and sleep well in your new home.

Categories

Recent Posts