Is the Las Vegas Housing Market Crashing | December 2025 Market Update

Is the Las Vegas Housing Market Crashing | December 2025 Market Update

🔥 The big headline: median price hit a record — but there's more to the story

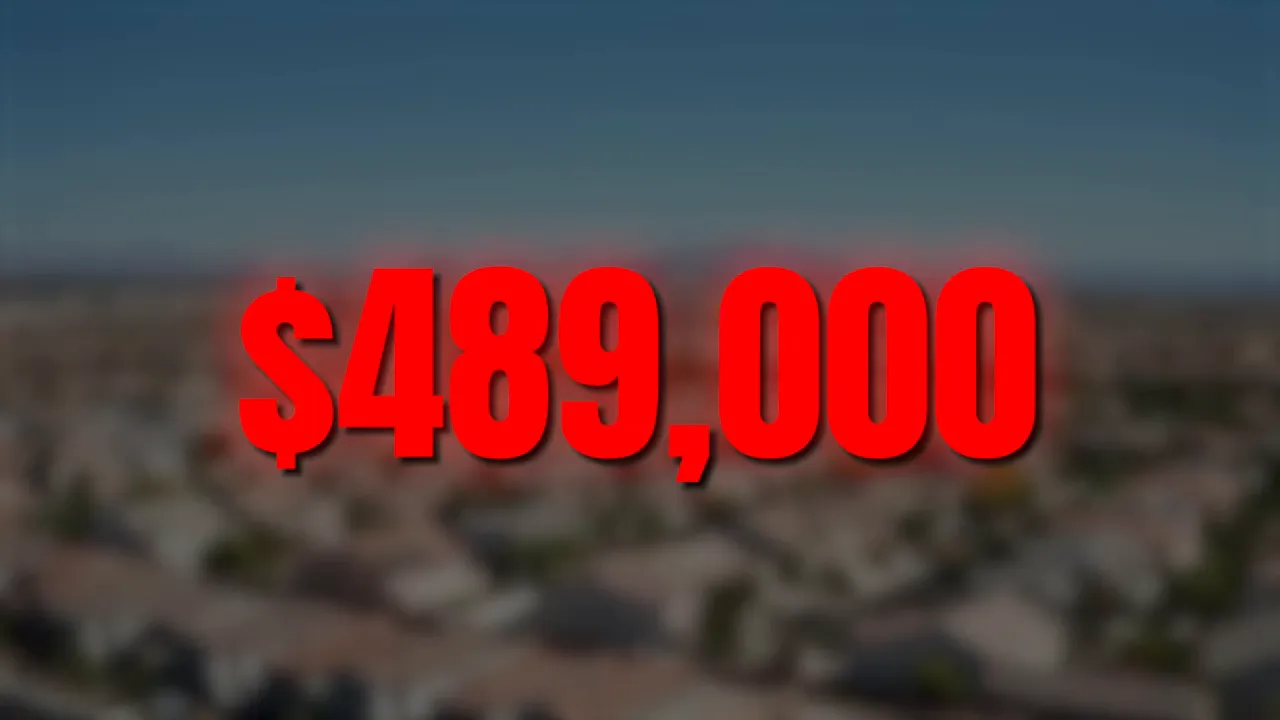

The median price for a single-family home in the Las Vegas Valley reached $488,995 in November 2025 — effectively $489,000 and up about 3.1% from October and 1.9% year-over-year. That number grabbed headlines, and for good reason: it's a fresh all-time high that makes people ask whether the market is overheating or about to collapse.

Numbers like that create a reflex: record price equals bubble. But median price is a summary statistic, and summary statistics hide details. The crucial detail this month is the mix of homes that actually sold.

📊 What the median price actually reflected

Only 1,538 single-family homes closed in November — that is down 10.8% from October and down 6.6% from November 2024. Fewer sales and a higher median means the composition of sales shifted toward higher-priced homes. Think of it like a car lot selling more luxury cars one month: the average sale jumps even if individual prices didn’t.

In plain terms:

- Higher-end homes made up a larger share of closings.

- Entry-level and mid-range segments slowed more noticeably.

- Your experience will depend heavily on price range and neighborhood.

📈 Inventory exploded — buyers are gaining leverage

Inventory is the part of the market that tells you what's changing now, not months later. As of the November report the valley had roughly around 7,300 single-family homes active on the market — about a 26.3% increase year-over-year. That pushed months of inventory for single-family homes to about 4.6 months, up from roughly 3.6 months last year.

Why does that matter?

- A balanced market is roughly 6 months of inventory. Below that favors sellers; above that favors buyers.

- At 4.6 months we’re moving toward balance. Sellers still have an edge in some pockets, but not like they did during the frenzy.

- Homes are sitting longer: only 47.4% of single-family homes sold within the first 30 days, down from 57.9% last year.

The upshot is negotiating power has shifted. Contingencies, inspections, repair requests, and seller concessions are back in play. That’s healthy. It slows the breakneck pace and pushes the market toward sustainable behavior.

🏘️ Where the market is different by neighborhood and price point

The valley is not a single market. I watch neighborhood-level trends closely because what’s true in Summerlin might not be true in North Las Vegas or Henderson.

- Henderson (in the $400k–$500k band): homes averaging about 40–50 days on market.

- Summerlin (higher end, over $600k): moving faster — closer to 20–30 days on market for many listings.

- North Las Vegas (first-time buyer band under $350k): surprising to see 50–60 days on average — still slower than pre-2020 craziness, but more choices for buyers.

Patience is an advantage today. Buyers don’t need to waive inspections to be competitive in many price ranges. Sellers who overprice from day one risk languishing and ultimately netting less than if they had priced correctly from the start.

🏢 Condos and townhomes: a clear buyer opportunity

Attached homes (condos and townhomes) tell a sharper story. Median sales price for attached homes sits around the low-to-mid $300,000s — a year-over-year bump of roughly 6% depending on the slice you watch. But the volume and supply numbers are the key here.

Here’s the picture:

- Only 380 attached homes closed in November, down 22.8% from October and down 20.2% year over year.

- Active inventory jumped to 2,613 units, a 40.8% increase year-over-year.

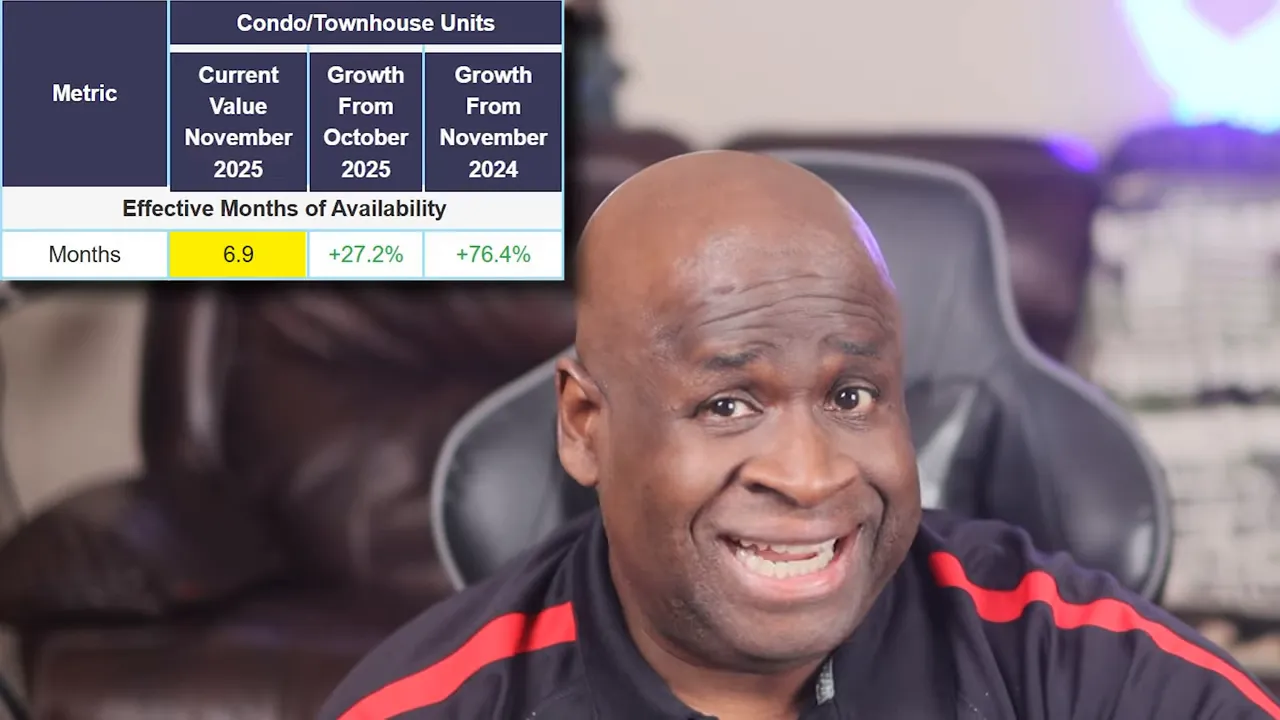

- That yields about 6.9 months of inventory — officially a buyer’s market for attached homes.

- Only about 43.2% of condos and townhomes sold within 30 days compared with 52.9% last year.

If you’re a first-time buyer, a military family looking near Nellis or Creech, or a young professional wanting affordability close to the Strip, the attached market is where negotiating power is clearest. Sellers are motivated, concessions are available, and you can be picky.

💸 Mortgage rates and affordability: context matters

The 30-year fixed rate was about 6.22% on December 11. That is higher than the pandemic-era lows but lower than the 2023 peak. The Federal Reserve did cut its benchmark rate to about 3.5–3.75%, but mortgage rates don’t move one-to-one with the Fed — they follow Treasury yields and investor demand.

Realistically, expect mortgage rates in the near term to hover between roughly 6% and 6.5%. Waiting for 4–5% may take a very long time.

A few practical affordability facts I emphasize:

- You do not need 20% down. FHA loans can be as low as 3.5% down. Conventional programs are available at 3% and some lenders offer zero-down options for qualifying buyers. VA loans remain zero-down for veterans and active-duty service members.

- Wages in Las Vegas are rising; the most recent data showed weekly wages are up about 7.6% year-over-year, which helps offset higher rates and prices.

- With more inventory, sellers are offering concessions again — closing cost help, repairs, and other flexibilities that improve affordability.

🏙️ Local economy: jobs, tourism, and why it matters for housing

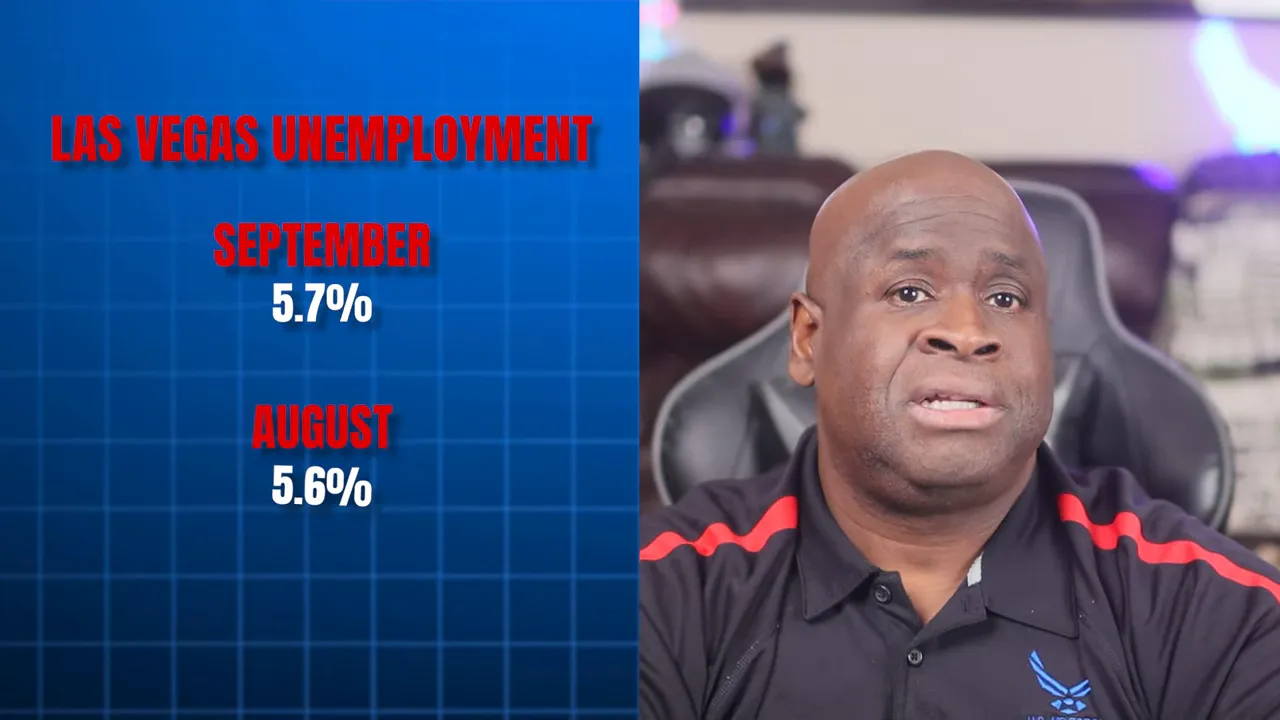

Las Vegas’s economy still leans heavily on tourism and hospitality, and those sectors soften when visitor counts slip. The unemployment rate ticked to about 5.7% in September, slightly above Nevada’s 5.3% average.

That number is elevated but not catastrophic. For perspective, Las Vegas hit 14% unemployment during the 2008 recession. Today the city’s economy is more diversified: data centers, logistics, technology relocations, healthcare, sports teams, and other sectors add resilience.

One constraint that matters for long-term housing supply: land. There are only roughly eight years of developable land left at current build rates. That scarcity will be a structural factor for longer-term price support.

🚫📉 Crash or normalization? The data-backed answer

Short answer: not a crash. Here’s why:

- Distressed inventory is tiny. The market had about 67 bank-owned properties and 59 short sales — roughly 126 distressed properties out of nearly 10,000 listings, about 1.3% of the market. Compare that to 2008 when distressed listings were a massive share of inventory.

- Homeowners have equity. Many buyers who purchased over the last 5–10 years hold significant equity. That prevents rushed, forced sales and the cascade of foreclosures that amplified the last crash.

- Lending standards are far stricter. Lenders now verify income, assess credit carefully, and underwrite to the borrower’s ability to repay. Subprime-style lending that fueled 2008 is not present at scale today.

What we are seeing is a healthy market correction: inventory rising from extreme shortages, sales cooling, negotiation power shifting back toward buyers, and prices normalizing after a period of rapid appreciation. That’s not the same as a collapse.

🛠️ Practical next steps — whether you're buying or selling

If you’re thinking about making a move in 2026, here are practical strategies I follow with clients.

For buyers

- Get prequalified and know your programs. Many buyers don’t realize there are low-down-payment options and down payment assistance programs. Veterans: check VA options. First-time buyers: FHA and conventional low-down options exist.

- Target the right segments. If affordability is the priority, look hard at condos and townhomes where months of inventory are highest and seller flexibility is strongest.

- Leverage time. You don’t have to waive contingencies to win in many neighborhoods. Use inspections and realistic offers to buy with protection.

- Be patient and picky. With more choices, you can wait for the right property rather than compromising heavily.

For sellers

- Price correctly from day one. Overpricing is no longer a safe bet. Homes that sit 60–90 days tend to sell for less than if priced right up front.

- Stage and market aggressively. Presentation and timing matter; homes that look move-in ready attract the better offers even in a cooling market.

- Be ready to negotiate. Expect inspection requests or closing cost help in many segments. Build concessions into your strategy if you want a timely sale.

🔮 What I’ll be watching in early 2026

Over the coming months I’ll be tracking:

- Mortgage rate movement and Treasury yields.

- Job growth and tourism trends — if hospitality jobs continue to decline it can pressure demand in certain neighborhoods.

- Inventory trends — does supply continue to rise toward six months or plateau?

- Buyer behavior in the entry-level segment — more choices there would be a significant shift for affordability in the valley.

❓FAQ

Is the Las Vegas housing market crashing?

No. The market is normalizing after several years of extreme seller advantage. Inventory is rising, sales have cooled, and negotiation power is shifting toward buyers in many segments, but the low level of distressed properties, widespread homeowner equity, and stricter lending standards distinguish this correction from a crash.

Should I buy now or wait for lower mortgage rates?

Waiting for a dramatic drop to the low 4s or 5s could take a long time. Mortgage rates have come down from 2023 highs but likely will stay in the 6–6.5% range for the near term. If your budget works today and you find a well-priced property with favorable terms, it can make sense to act rather than wait for uncertain rate movement.

Is the condo market a buyer’s market?

Yes. Attached homes currently show about 6.9 months of inventory and a sharp year-over-year inventory increase. That puts condos and townhomes clearly in buyer-favored territory, with more negotiating room and opportunities for concessions.

Do I need 20% down to buy in Las Vegas?

No. Many programs let you buy with much less cash down: FHA (3.5%), conventional (as low as 3%), VA loans (often zero down for qualifying veterans or active-duty service members), and some down payment assistance programs. Speak with a loan officer to understand options for your situation.

Are foreclosures flooding the market?

No. Distressed listings are a very small portion of inventory — about 126 bank-owned or short-sale properties out of nearly 10,000 listings, roughly 1.3% of the market. That is far from the conditions that created the last crash.

✅ Final thoughts

Las Vegas is moving from an overheated seller’s market toward more balance. Record median prices coexist with falling sales and surging inventory because higher-priced homes accounted for a larger share of closings. That distinction matters if you’re making decisions.

If you’re buying, you have options and time to negotiate. If you’re selling, price and presentation are essential. The market is not collapsing — it is normalizing, and that creates opportunities for well-informed buyers and disciplined sellers.

I’ll be publishing a follow-up report that lays out specific strategies for buyers and sellers and five predictions for 2026. Until then, focus on the numbers that matter today: months of inventory, days on market, mortgage rates you can lock in, and the affordability programs you can use.

Categories

Recent Posts